Staying Ahead of the Curve

At the end of January, the so-called Magnificent 7 reported earnings that were good, but not good enough in view of the growth expected by sky-high price earnings ratios averaging 78.5. The reactions were mixed and the group has been flat so far this year. In 2025, the Magnificent 7 -- Nvidia, Apple, Microsoft, Amazon, Alphabet Class A (Google Class A & C), Tesla, Meta Platforms Class A, and Broadcom – did very well and comprised 37.7 percent of the S&P 500 Index because of the heavy capitalization weighting. The S&P 500 Index rose 16.4 percent in 2025, but without the Magnificent 7 it only rose 2.9 percent. Staying Ahead of the Crowd SoundAdvice Advising Investors for 37+ years www.soundadvice-newsletter.com Febuary 2026 Issue January 30, 2026 The Magnificent 7 stocks have been pumped up by the AI boom. There is little doubt that AI is changing the world, but it is prompting billions of capital expenditures into data centers, chips, infrastructure, and AI related equipment. Yet, there is not a clear picture of when and how much of a payout is ahead. If the investment return on the billions these companies are spending does not meet expectations in a timely fashion, the future of these stocks, as well as the S&P 500 Index, is questionable at best. However, that is not the case for the rest of the stock market. Nearly every sector of the economy is already benefiting from AI applications and AI is bound to provide widespread efficiencies. Consequentially, it makes more sense to invest in companies whose earnings will benefit from AI services and whose stocks are reasonably valued. As AI fuels efficiencies and boosts earnings in virtually every industry, the bull market is bound to broaden out. One obvious beneficiary of this trend is the Invesco S&P 500 Equal Weight ETF (RSP)

The Sound Advice Risk Indicator

Another sign that the S&P 500 Index is inflated is revealed from the Sound Advice Risk Indicator, which compares the Index to house prices for 130 years. The latest reading is 2.51, which puts the S&P 500 Index above the highrisk watermark of 2.0.

Our Risk Indicator identifies supercycles, the solemn, inexorable seasons that roll across the market’s landscape; there

will be no heat waves in January, no blizzards in July. But in our search for fair winds, we need to know more than the

season. We also must be able to predict the shorter-term weather -- the business cycles behind the bull and bear markets that fluctuate along the path of supercycles.

The Sound Advice Diffusion Indexes

We rely on the Sound Advice Diffusion Indexes to identify business cycles because they have an accurate track record of predicting major stock market trends for the last 50+ years. They work by observing changes in the most sensitive leading and lagging economic indicators that lead to shifts in interest rates. During “Aggressive” signals over the last 50 years, the S&P 500 climbed an average of 31.5 percent. The market has undergone corrections but has never crashed. All market crashes have occurred during “Caution” signals. When the stock market was not crashing, the S&P 500 either meandered, climbed moderately, or declined in an extended bear market, recording an average decline of 0.6 percent.

The most recent signal change was in late 2022, when our Diffusion Index of Leading Indicators recorded a zero reading which led to a new signal change from “Caution” to “Aggressive”. That signal was prescient as we began a new bull market.

The next signal will come from a 100 percent reading of our Diffusion Index of Lagging indicators, revealing that the economy is overheating and exerting upward pressure on inflation and short-term interest rates. It would take a seismic increase in all of the underlying economic indicators contained in our Diffusion Index of Lagging Indicators to cause a 100 percent reading. Accordingly, the end of the current bull market is not on the horizon, and, for the reasons stated above, it should broaden out to benefit more and more stocks that are held by diversified portfolios.

The Sound Advice Recomendations

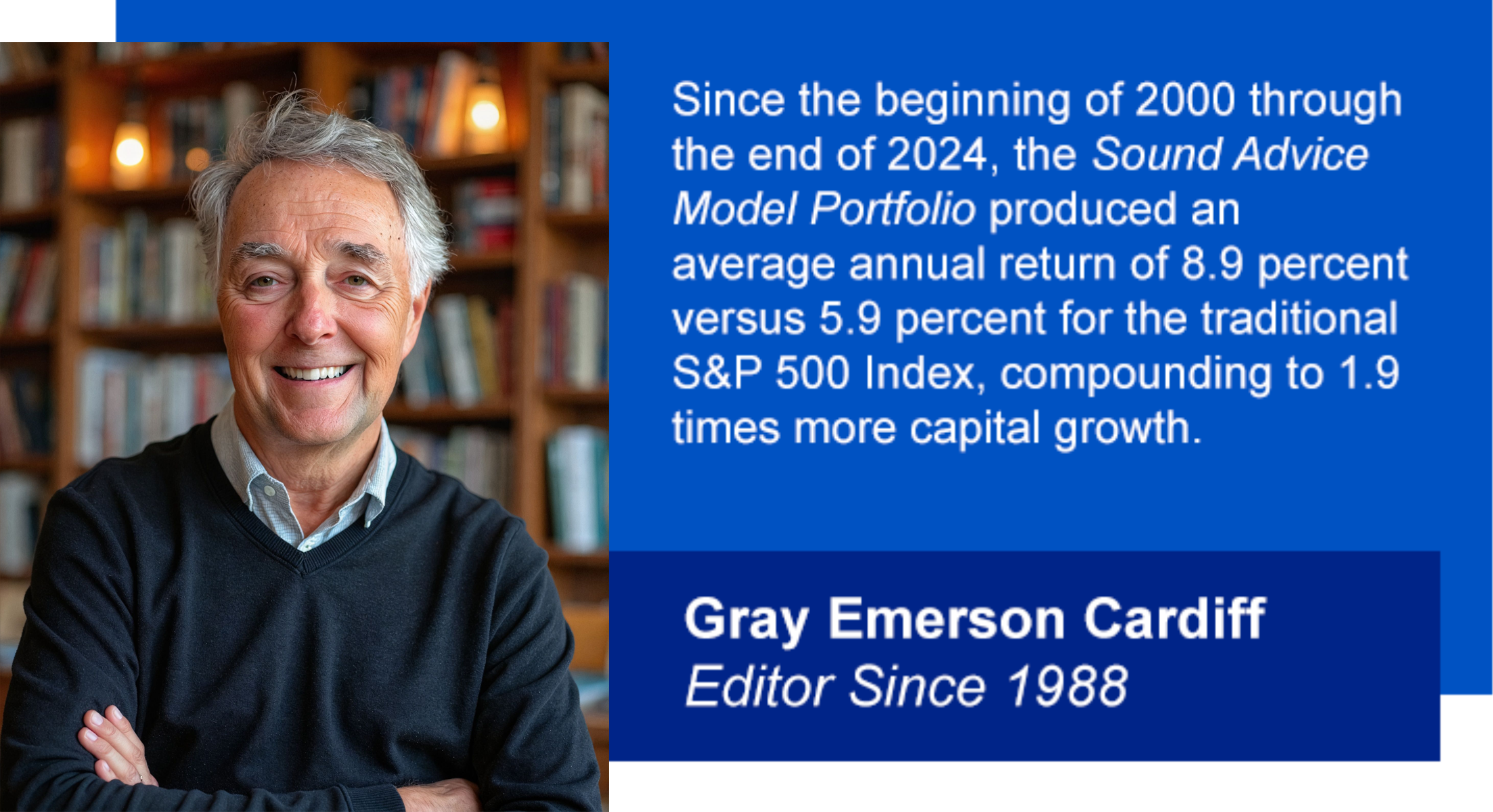

We eat our own cooking. The Sound Advice Diversified Growth Fund invests exclusively in the Sound Advice Model

Portfolio recommendations. The editor of Sound Advice for 36+ years, Gray Cardiff, manages the Sound Advice Fund and

is also an investor on a side-by-side basis with the other investors. You can request a prospectus for Sound Advice Fund

on the log-in page you used to download this issue of Sound Advice.

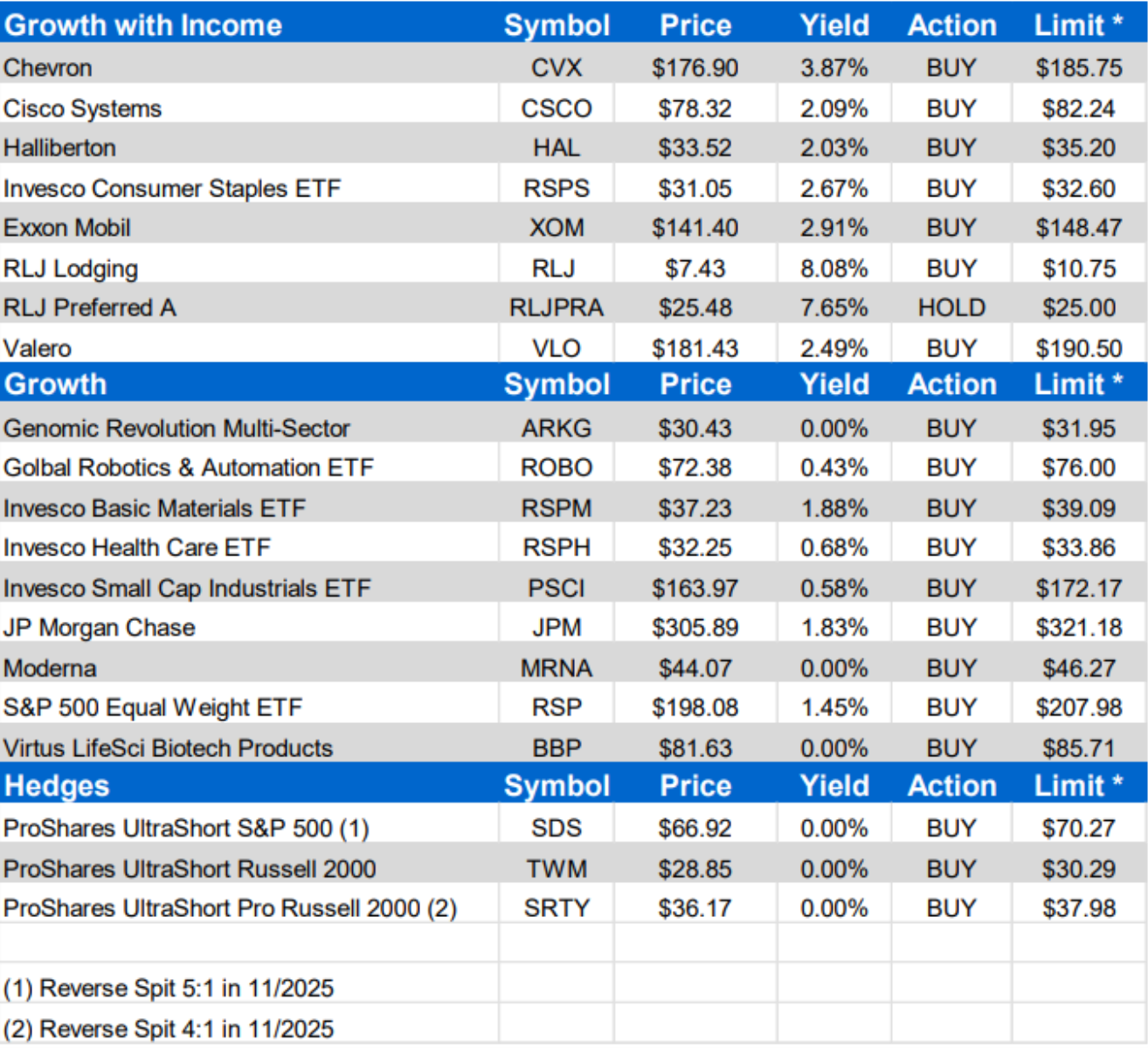

The Model Portfolio

Our individual stock recommendations are special situations offering a compelling value proposition. We are also recommending liquid electronically traded funds (ETFs) investing in sectors that are bound to benefit in the months and years

ahead. All recommendations, as well as their dividend yields and buy/hold/sell recommendations, are summarized in the

table and sorted by investment objective categories and then in alphabetical order.

Downside Hedges

We include downside hedges as part of the portfolio to reduce risk and dampen volatility by profiting during market corrections. Minimizing losses, even at the expense of limiting the upside, has been our key strategy for outperforming the

market over the long run

ProShares UltraShort S&P 500 (SDS) is designed to produce two times the daily fluctuations of the traditional S&P

500 Index, only in reverse. For example, a decline of say,1.0 percent in the Index will cause SDS to increase by 2.0

percent. Conversely, an increase in the Index will cause SDS to decline by 2.0 percent. We are including SDS as a hedge

because the S&P 500 Index is distorted and inflated, as discussed above.

As with any variable, there is a way to gain perspective on what the most likely range will be in the months ahead. It is

a basic statistical calculation called the standard deviation, which measures the amount that a variable typically deviates

from its average (mean) during a defined period. The high and low boundary within which the variable has moved for 68

percent of the time is statistically defined as one standard deviation, which is deemed to be the most likely range for the

future.

Since the depths of the Great Financial Crisis in 2009, the P/E of the S&P 500 Index averaged P/E of 22.4 with a

standard deviation of 5.0. This means that the P/E has been within 17.3 to 27.5 for 68 percent of the time. Applying

this standard deviation P/E range to on today’s earnings of the S&P 500 Index of $256.35, the future range of the

S&P 500 Index puts the range from a low of 4,436 to a high of 7,227. At the average P/E, the S&P 500 Index would

be 5,354 which is 17.2 percent lower than today’s closing. Accordingly, here more potential on the downside than the

upside.

The Russell 2000 Index

The Russell Index is comprised of small and mid-sized domestic companies which tend to be more volatile than the

overall market, especially during market corrections. The following two ETFs below can also be used as a downside

hedge because they short sell the Russell 2000 index. They differ in the leverage employed, which you can choose

one according to your investment objectives and risk tolerance.

ProShares UltraShort Russell2000 (TWM) is designed to produce two times the daily fluctuations of the Russell

2000 index (IWM). A decline of say,1.0 percent in the Russell 2000 will cause TWM to increase by 2.0 percent. Conversely, an increase in the Russell 2000 will cause TWM to decline in the same fashion.

ProShares UltraShort Pro Russell2000 (SRTY) is designed to produce three times the daily fluctuations of the

Russell 2000 index.

Special Situations

The following stocks are individual companies presenting extraordinary values within their respective industries.

Here they are in alphabetical order:

Cisco Systems (CSCO) is a value play in the AI boom because it supplies the backbone of data center networking equipment and software. The upside growth potential is not anticipated by the current stock price, as evidenced

by a relatively low P/E and an attractive dividend yield. CSCO is a direct beneficiary of the billions of capital spending

slated for data centers and AI related equipment. Cisco’s management is reporting strong AI business growth and is

confident that AI will continue to be a driver of growth.

JP Morgan Chase (JPM) is a good value for what is considered the world’s highest quality banking enterprise with

diversified businesses and prudent underwriting policies. Deregulation of the industry will continue to be a substantial

benefit to JPM. The Company has a long history of growing dividends. At the recent Goldman conference, JPM said

that productivity in operations is improving because of AI programs could be scaled further

Moderna (MRNA) is a pure investment play on Messenger RNA (mRNA) technology. This revolutionary technology

is on a path to provide solutions for not only vaccines, but for cures and treatments for the most deadly and debilitating

diseases haunting humanity. Management believes that the company’s cash reserves will be sufficient to sustain the

business while it develops vaccines and treatments.

After Phase 2 results showed a 75% recurrence free survival rate after three years, the mRNA-4157 cancer vaccine

is now in a Phase 3 trial for adjuvant melanoma. In January, the company announced 5-year results from its phase 2b

study of this cancer vaccine in melanoma patients of a 49% reduction in the risk of death or recurrence at five years.

There are also other promising cancer vaccines in the pipeline including a vaccine for renal call carcinoma.

Moderna is working on personal cancer vaccines through the use of analyzing see fragments of cancer cells in a

blood draw, allowing the detection of cancer in early stages, before it graduates into more serious later stages. Data

will be transmitted through the cloud to Moderna’s IT system, and AI algorithms will be used to compare an individual’s

particular cancer cell mutation to the hundreds of thousands of possibilities and to the treatments that are currently

effective. Management says Moderna will be able to analyze and develop a treatment customized for an individual patient within 30 days of the blood draw, and over time with more and more data, the process will become more efficient

and accurate.

RLJ Lodging Trust (RLJ) pays an annual dividend of 60 cents per share is a yield of 7.8 percent, and the dividend

is well-covered by the company’s cash flow. This REIT is severely undervalued.

RLJ has a large and diversified portfolio of hotel properties, with 96 premium-branded, high-margin, focused-service

and compact full-service hotels located in 23 states and Washington DC. This is a low-leveraged REIT because the

company’s debt is only 46 percent of its (book value) assets.

The portfolio’s net operating income (NOI) for the trailing four quarters was $380 million. Using a conservatively

high cap rate of 7.5 percent produces a portfolio value of $5.07 billion. Adding other assets and subtracting liabilities

leaves the company equity of $3.09 billion. After subtracting the liquidation value of the company’s only preferred stock of $328 million leaves equity for the common shareholders of $2.76 billion. Dividing that equity by the 149.5 million

shares of RLJ outstanding translates to a net asset value of $18.46 per share – more than double the current price of

the stock price.

RLJ’s $1.95 Series A Cumulative Convertible Preferred (RLJPRA) is RLJ’s only preferred stock, with a liquidation

preference of $25 per share, which is the maximum value that would be received from an acquisition of the company.

Use limit orders at $25 or lower to accumulate this preferred stock for a safe annual yield close to 8 percent. The dividends for this preferred only consume 10.2 percent of the company’s cash income and must be paid before common

dividends, making the yield highly secure.

Special Situations in Energy

As the US flotilla sailed from Venezuela to Iran at the end of January, Iran warned that it intends to carry out a naval

exercise involving live fire in the Strait of Hormuz imminently, one of the world’s most critical oil transit routes used by

close to 20% of global oil flows. The price of oil and gas had been on the rise and spiked in the ending days of January. As a result, the prices of our energy holdings have risen sharply.

Looking beyond the near-term crisis in Iran, world-wide supplies are adequate, even without Iran’s 3 percent contribution. However, increasing volume coming from the US to the rest of the world will increase revenue for the major US

oil companies, even without high energy prices.

Energy providers also stand to benefit from the AI boom. Power needs from data centers is expected to double by

2030 after decades of stagnant demand in the US.

Our following energy selections present stellar values for long-term profits with currently attractive and potentially

increasing already attractive dividend income.

Chevron (CVX) reported earnings at the end of January that beat expectations on both gross revenue and earnings.

has a long history of dividend increases. Future dividend increases are bound to be supported by production growth

from assets in the Permian Basin. The acquisition of Hess Corporation (HES) in July 2025 gave the company a 30%

share in the Guyana Stabroek block which holds the equivalent of 11 billion barrels with a low production cost. Chevron’s daily production has risen above 4 million barrels.

Chevron has a strong balance sheet with low debt, which along with plenty of free cash flow, give it staying power

during adverse conditions with the ability to make timely accretive acquisitions.

Chevron recently announced that it plans to build its first project to power an AI data center using natural gas in West

Texas which is planned to provide 2.5 gigawatts of off-grid power.

Exxon Mobil (XOM) has low production costs. Production from its immense Guyana field it shares with Chevron

is boosting earnings despite lower oil prices and lower refining margins. The benefits are starting to appear from

the 2023 acquisition of Pioneer National Resources, evidenced by new production growth in the Permian Basin. XOM

also has an attractive dividend yield with a history of dividend increases. The dividend was increased again in 2025 for

a solid string of 43 annual dividend increases.

Exxon will certainly participate in developing the massive proven oil reserves that reside in Venezuela because of its

experience and expertise in developing oil assets in the region.

Halliburton (HAL) is a premier oil field services company. With a substantial presence in the US, Halliburton derives a larger share of its revenues from North America than its primary competitors, SLB Inc and Baker Hughes. The

world’s easy oil reservoirs have been developed, even in the Middle-East. Now it takes more sophisticated equipment

and technology, which is what Haliburton provides. That trend puts HAL on a growth path.

Halliburton has technological innovations that are tailor made for the unconventional reservoirs in the US, including

its directional drilling system, the iCruise CX system, which is a rotary steerable tool and LOGIX drilling automation

platform that makes it possible to reliably drill in curves and laterally in a single run. This new technology has been

rapidly deployed in the Permian Basin.

Other relatively new Halliburton technologies include the Zeus platform, electric pumping units, Octiv Auto Frac, and

Sensori subsurface measurement. These systems increase efficiency and replace outdated and costly diesel generators as power sources for onsite drilling with generators capable of using natural gas, LNG, and a variety of other fuels

that are available on the drilling site.

In Alaska, where some of the nation’s largest oil and gas reserves reside, Halliburton’s EarthStar ultra-deep resistivity tool and reservoir mapping service delivers unmatched performance on the North Slope. Exploring in Alaska was

curtailed by the Biden Administration, but that is now expanding under the Trump Administration.

Valero Energy (VLO) was added to the portfolio several years ago at $60.41 per share. As earnings have grown,

VLO is still a bargain with a relatively low P/E and attractive dividend yield. Valero makes its money from the “crack

spread”, which is the profit margin derived from purchasing crude oil, turning it into refined products such as gasoline

and jet fuel, and selling those refined products.

Valero has the unique ability to refine both light crude oil coming from fracking in the US Permian basin as well as the

sticky heavy crude coming from Venezuela. Light crude oil is great for refining into gasoline but not much else. Heavy

crude is sought by refiners because it refines into many other products at high profit margins, ranging from diesel fuel to

asphalt. Access to Venezuelan crude will benefit VLO over the longer term when production there increases.

Valero’s ability to refine a variety of crude oil types also gives it the ability to achieve discounts for its crude oil feedstocks. This flexibility and access allow Valero to capture the highest margins among its competitors because it can

take advantage of the temporary gluts of crude, whether it’s low or high-quality crude or light sweet (low sulfur) or

heavy sour (high sulfur) crude, to obtain the best available discounts for its feedstocks. The company’s refineries also

have access to the US pipeline network from its gulf coast locations.

Valero’s “green energy” joint venture with Diamond Green Diesel is producing renewable diesel at large profit margins. Renewable diesel is made from animal or plant waste material which reduces greenhouse gas emissions up to 80

percent because it only releases as much carbon dioxide as the material originally contained. Renewable diesel does

not congeal at low temperatures which means it can be easily transported through pipelines.

Equal Weight S&P 500 ETF